Market Views, Data Centre | Demand outpaces supply as AI puts the Norwegian market in focus

Power constraints across Europe and the emergence of AI factories have, in just a few years, placed Norway firmly on the map for some of the world’s leading data centre developers. Four years have passed since the first AI wave reached the Norwegian market, and growth has continued at a rapid pace. Today, ambitions and option agreements are beginning to materialise into large-scale construction projects.

The main limiting factor is the power grid, and increasingly so. Major grid infrastructure investments are time-consuming, and the application queue for grid connections has grown rapidly. Akershus Eiendom’s analysis indicates that approximately half of the projects in the power queue are being developed by players with the execution capability and capital sources required to build and own the data centres themselves.

AI boom and demand growth

From a market historically dominated by smaller, local data centres, Norway is emerging as a platform for some of Europe’s most ambitious data centre schemes. This shift is driven by rapidly increasing demand for compute capacity, particularly related to artificial intelligence from neocloud operators and self-build users. Demand from hyperscale players such as Microsoft and Google, which are already established in Norway, has also increased significantly against the backdrop of an even more acute power situation in Europe’s largest data centre markets.

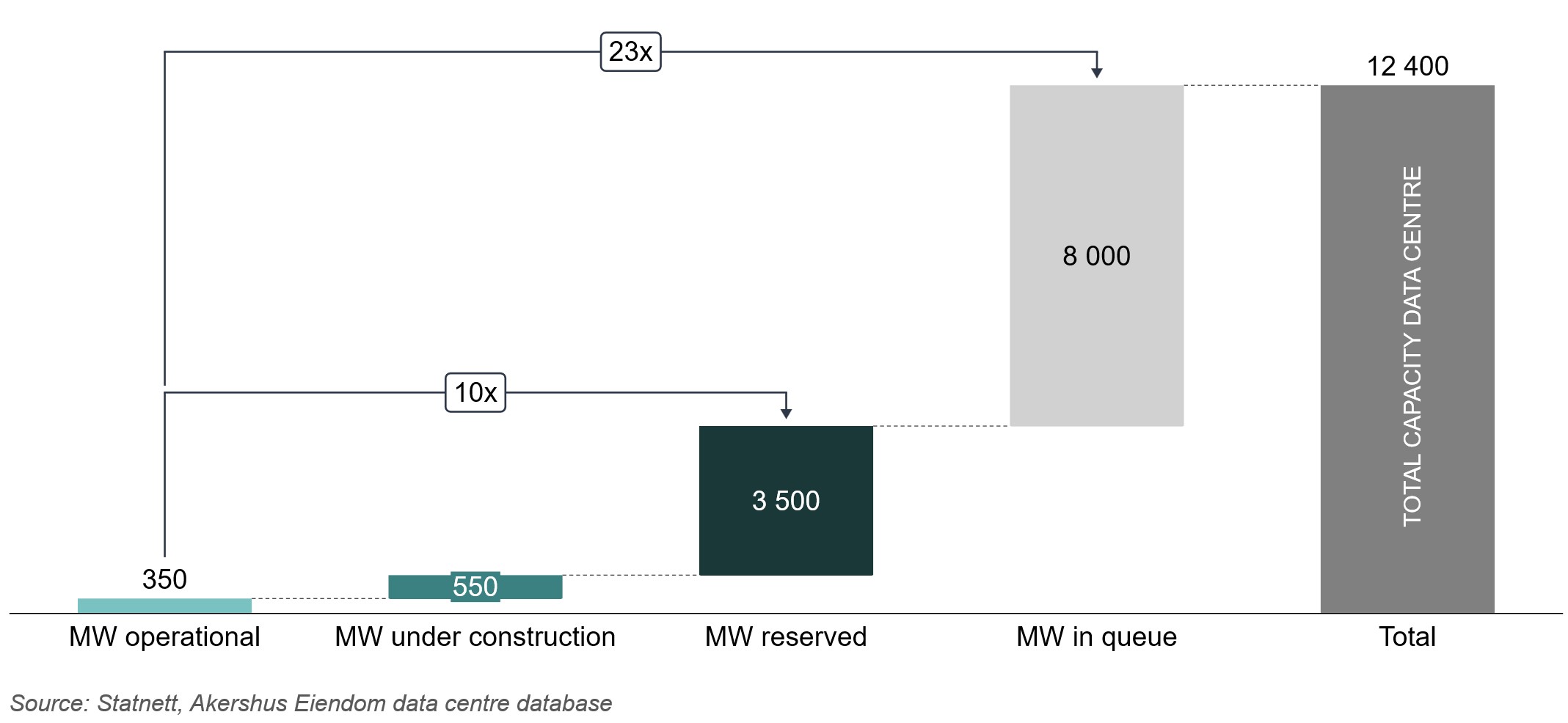

Akershus Eiendom’s analysis shows that the pipeline of projects that have secured reserved grid capacity is currently ten times larger than all operational data centres in Norway combined. The pipeline of mature projects awaiting assessment by Statnett is as much as 23 times larger than the existing market.

The Norwegian market is therefore caught between major long-term infrastructure projects in the national power grid and the rapid public adoption of Claude, ChatGPT and far more advanced AI services.

Figure 1: MW operational, MW under construction, MW reserved and MW in queue

Scarcity is changing the rules of the game

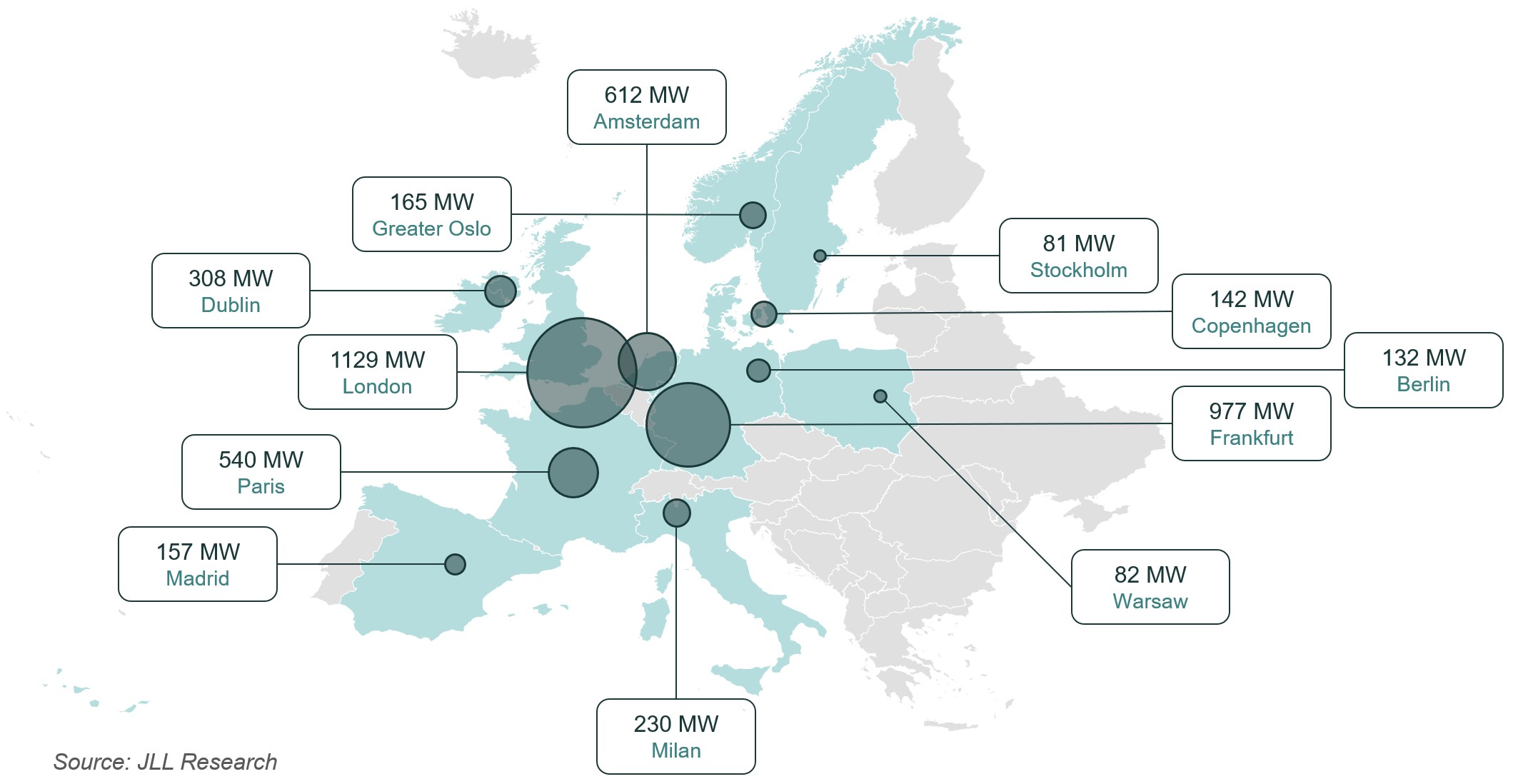

Both in Norway and across the major European markets, there is now very limited available capacity in existing data centres. In the five major markets, collectively referred to as FLAP-D1, vacancy has fallen from close to 20 percent to 6 percent over five years, despite substantial new data centre supply being delivered over the same period.

1 FLAP-D: Frankfurt, London, Amsterdam, Paris, Dublin

The scarcity of existing data centre capacity has forced the market to take a longer-term view. As much as 83 percent of capacity currently under construction in the FLAP-D markets has already been pre-let before completion. Contiguous capacity of 10 MW or more is effectively unavailable in existing buildings, and occupiers looking to secure space must commit long before the requirement actually materialises. This is pushing rents upwards. Rents in Europe’s primary markets have increased by around 40 percent since 2022.

In Norway, rents for certain contract types have increased even more, albeit from a lower base. Liquidity in Norway is, however, significantly lower than in other European markets, and the strong rental growth experienced by several market participants is difficult to substantiate with anything other than anecdotal evidence. As of 2026, the Greater Oslo data centre market is approximately 10–15 percent of the London market.

Figure 2: Primary and secondary data centre markets in Europe (MW)

Fully let new-build schemes

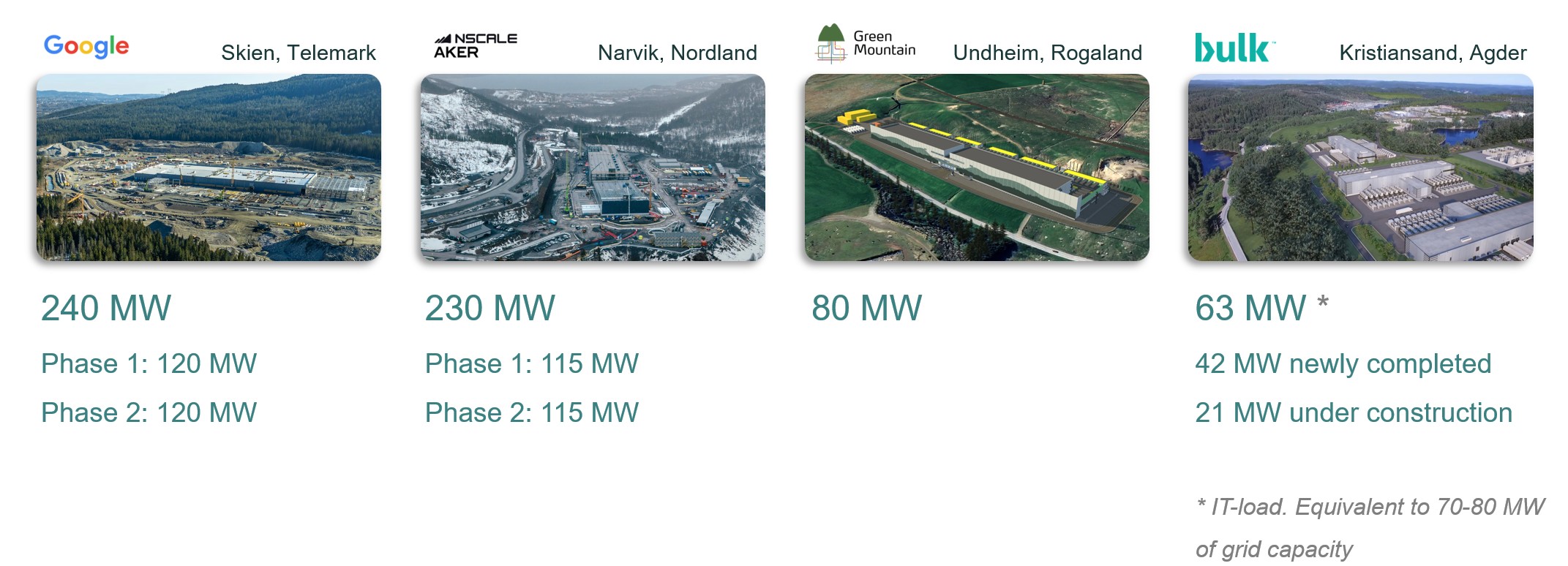

The leasing trend towards long-term commitments in new development projects is at least as evident in Norway as in the larger European markets. Some of the largest centres currently under construction in Norway are, for all practical purposes, fully committed. Google will use all capacity in Skien itself. Nscale is filling its Narvik centre with its own servers and has an agreement with OpenAI for the lease of compute capacity. Green Mountain’s centre at Undheim in Rogaland is let to one large international occupier.

Figure 3: Major projects under construction in Norway

Positioning for scarce grid capacity

The Norwegian data centre market has increasingly become a positioning game for access to power. Demand for grid capacity is high, while actual available capacity in the transmission and regional grids is limited. For players seeking to establish data centres in Norway, the market is therefore not only about identifying suitable sites, but in practice about securing reserved grid capacity before competing projects do.

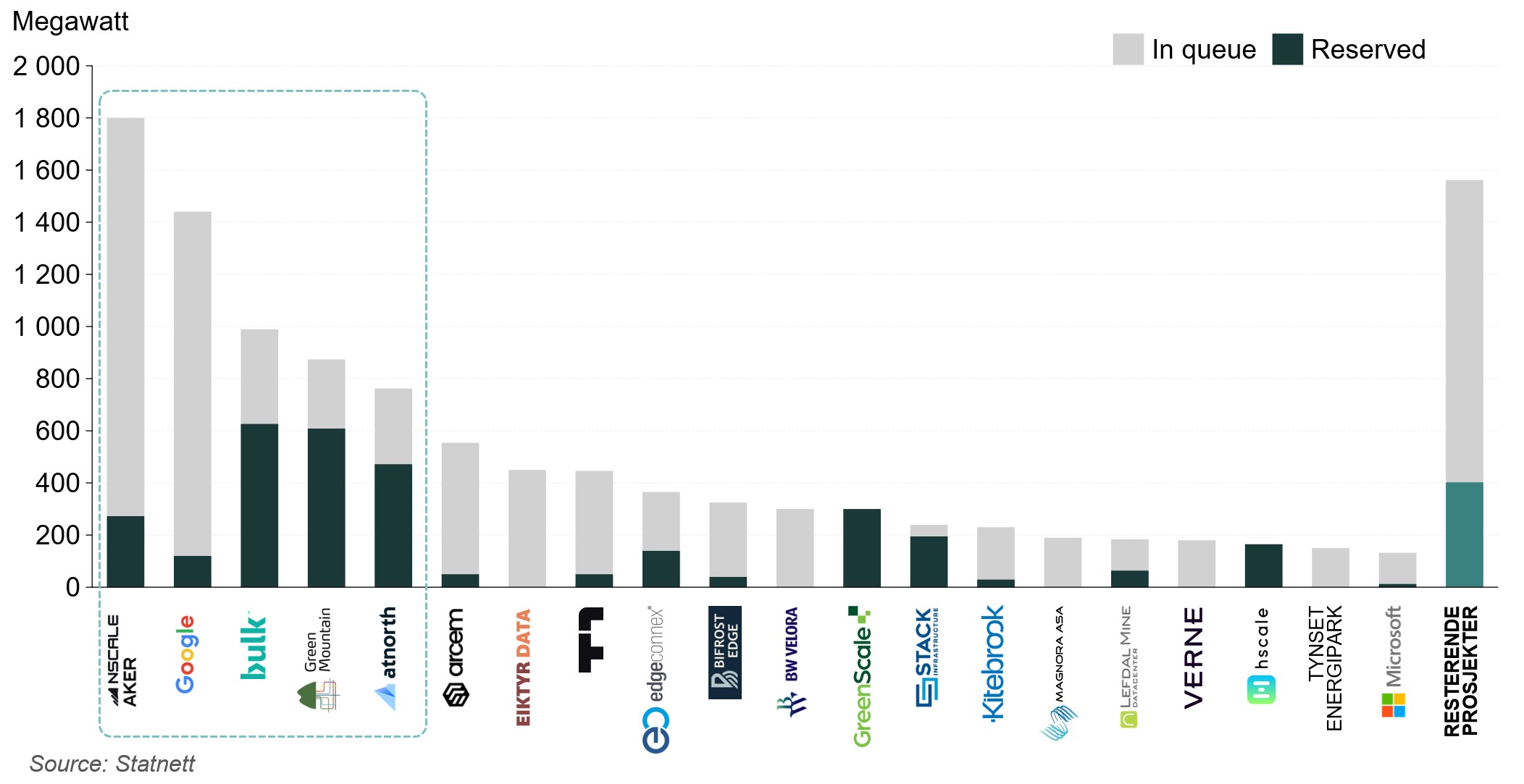

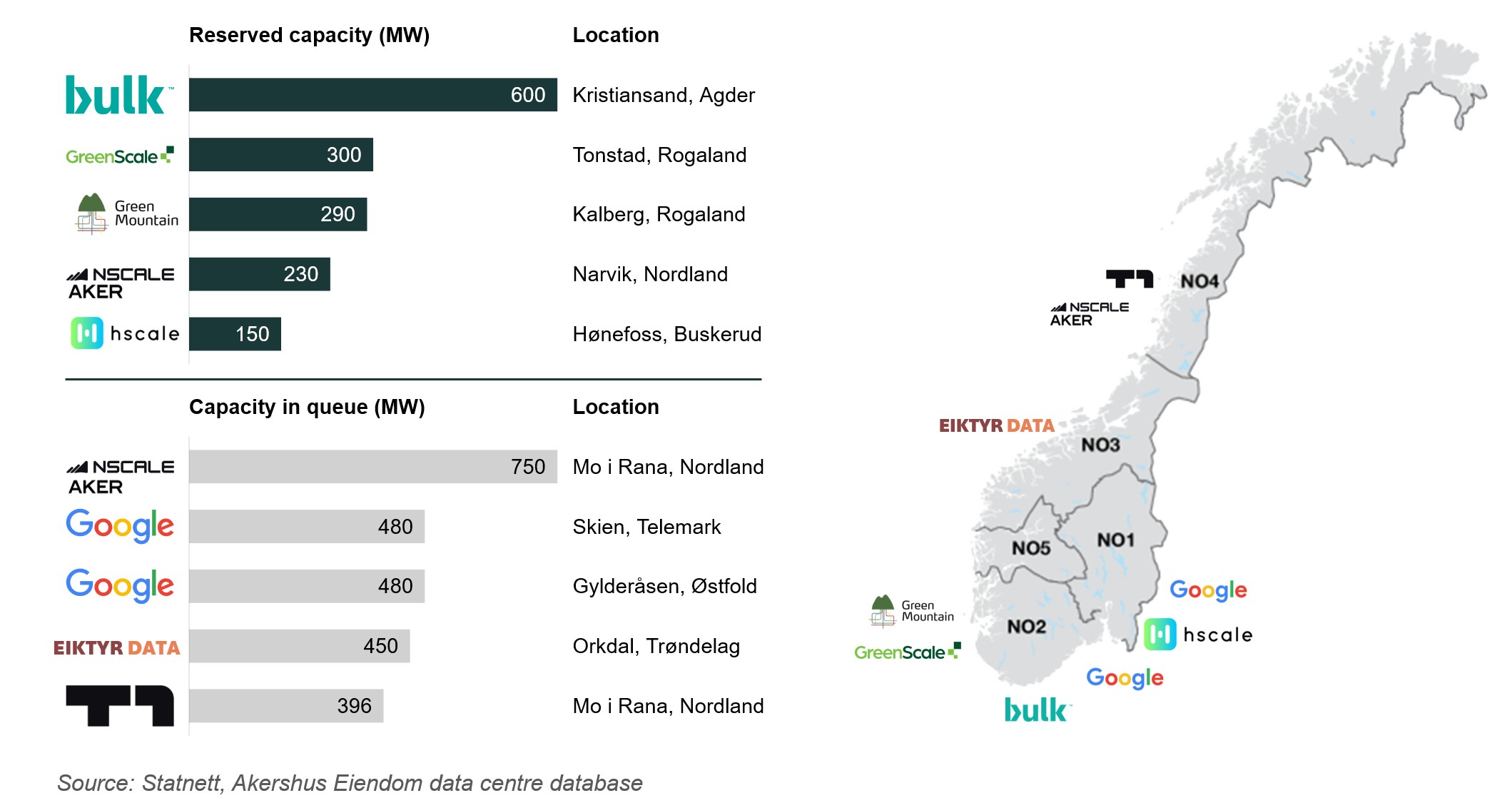

Among the largest players in the capacity queue are Nscale (Aker), Google, Bulk Infrastructure, Green Mountain and atNorth. Combined, these five players account for as much requested capacity as the next 52 players in the queue put together.

Figure 4: Reserved grid capacity and capacity in queue

A small number of major players dominate the grid queue

The projects launched over the past three years are on an entirely different scale from anything the Norwegian market has historically handled. Today’s project pipeline is largely dominated by AI and hyperscale schemes with very high-power requirements. According to Akershus Eiendom’s estimates, the ten largest projects awaiting grid capacity represent a total construction cost of approximately NOK 500 billion. The aggregate power requirement for these projects is roughly equivalent to Norway’s net power exports via interconnectors in 20252. However, we observe that only a few of these projects have secured committed grid capacity. Among the most prominent projects are:

2 In 2025, Norway’s gross electricity exports amounted to 34.4 TWh, while net electricity exports totalled 22.8 TWh. This corresponded to approximately 21% and 14% of Norway’s total electricity production the same year, respectively.

Figure 5: Ten largest data centre projects with reserved capacity and capacity in queue

Stricter requirements for larger projects

For larger power-intensive data centre projects, Statnett has introduced stricter maturity requirements for grid connections above 100 MW. The purpose is to ensure that limited grid capacity is prioritised for projects with sufficient progress, documentation and execution capability. DLA Piper has commented further on this in part 2 of the analysis.

Read DLA Piper’s article on the grid connection process and new maturity requirements here.

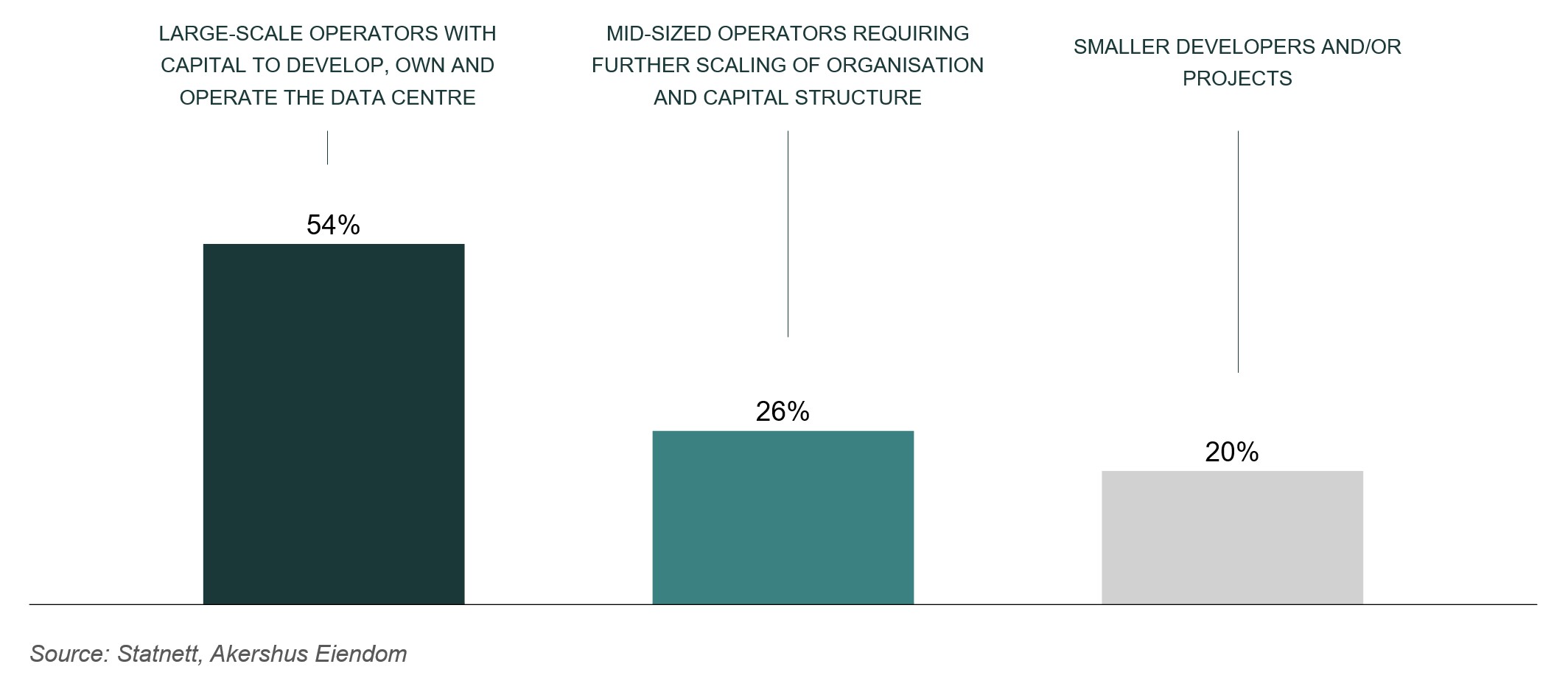

In a new analysis, Akershus Eiendom has assessed each project and organisation with reserved capacity and capacity in Statnett’s queue. Based on this analysis, approximately 54 percent of projects, measured in megawatts, are assessed as having the execution capability and access to capital required to develop and own the data centre projects they have launched. These players have proven execution capability either in Norway or internationally. 26 percent can advance their projects to construction independently, but the scale of their project will require them to expand the organisation and bring in a new capital partner. A partnership with a more mature player may be a natural route. The remaining 20 percent are assessed as projects with a lean organisation and no known data centre projects to reference. Several appear to have the capital required to bring the project to shovel-ready status, but not the multibillion-NOK capital required to develop the planned data centre. It should be noted that there may be partnership agreements behind some of these projects that have not yet been announced, as the projects are at an early stage.

Figure 6: Assessment of data centre projects with reserved capacity and capacity in queue

Data centres as the main driver of pressure on the power grid

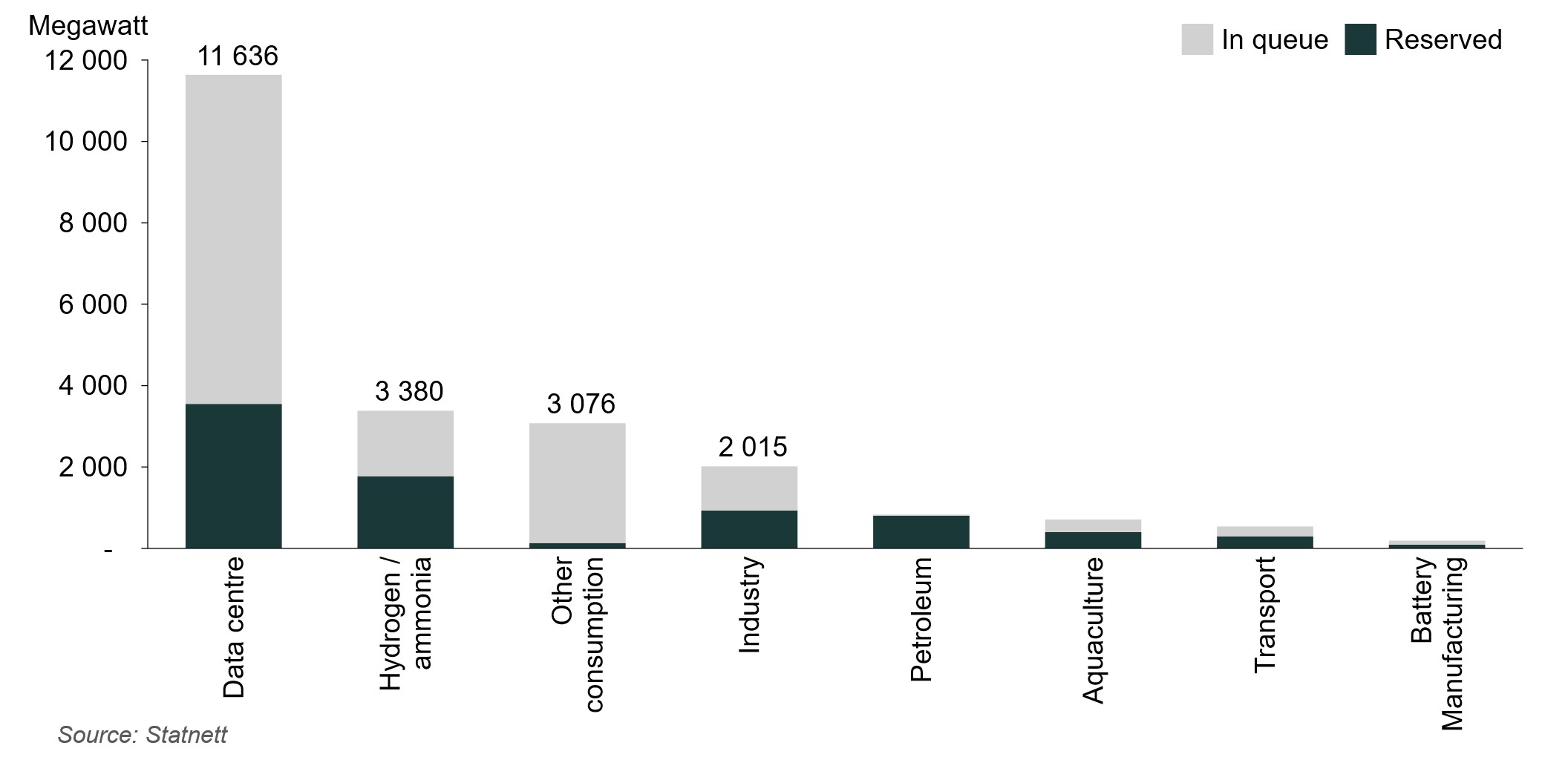

Data centres have become by far the largest single source of pressure on the Norwegian power grid. Of all capacity currently in Statnett’s queue, approximately half, or 11,636 MW, relates to data centre projects alone. By comparison, hydrogen and ammonia account for 3,380 MW, other consumption for 3,076 MW and traditional industry for only 2,015 MW.

Figure 7: Half of all reserved grid capacity and capacity in queue comes from data centres

This picture is nevertheless nuanced by the fact that significant capacity has been withdrawn from the queue since 2022. According to Statnett, approximately 4,500 MW has been removed from the capacity queue, largely related to green industrial projects. Players such as Yara, Inovyn, Vianode and Ineos have terminated grid capacity agreements in the Grenland area. Statnett also does not expect today’s large hydrogen projects to be realised to the same extent as previously assumed. As a result, data centre players are likely to increasingly compete for capacity that was previously intended for other power-intensive industries.

Value of powered land in Europe vs Norway

Demand growth in the major European markets has had a substantial impact on land values for so-called powered land. This is a collective term for sites with secured grid capacity that can be sold as a package for power-intensive industrial development.

The Norwegian grid connection system requires the end-user of the power to apply for grid access. A landowner cannot apply before there is a real project, and the project cannot apply before it has access to a site. This creates a chicken-and-egg situation where, over time, market practice has developed around entering into option agreements or conditional purchase agreements linked to power and zoning, with the site being acquired once grid access has been secured. Norway is not alone in facing this challenge, but other systems place more control in the hands of the landowner.

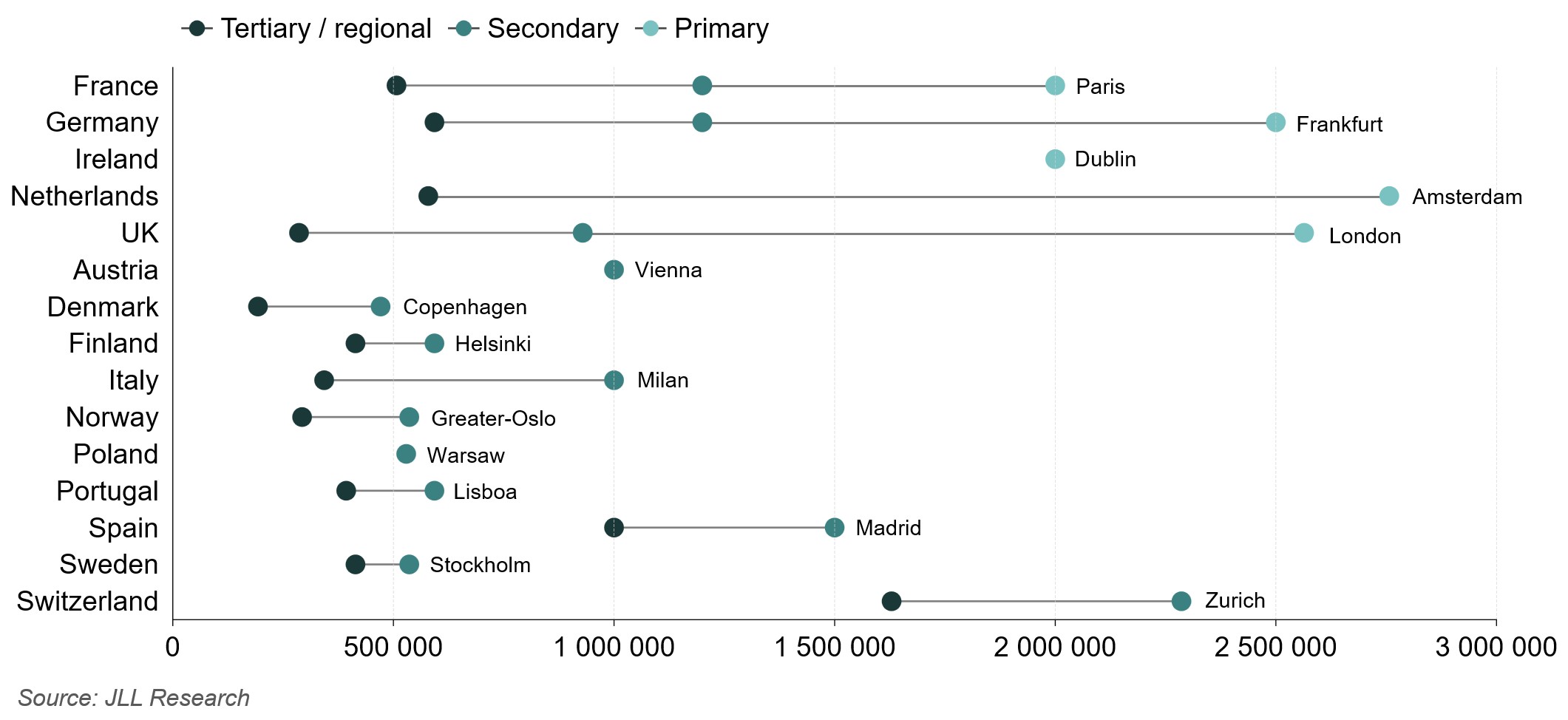

Differences in demand for data capacity, combined with differences in grid connection regimes, create significant variations in the value of powered land. Akershus Eiendom’s international partner, JLL, finds that sites with power access in primary markets achieve, on average, 1.8 times higher values than secondary markets and 3.1 times higher values than tertiary markets.

Figure 8: JLL powered land comparables, euros (€) per MW IT

Value drivers for land in Norway: Where are the opportunities?

Far from all industrial parks in Norway are attractive for data centre development. Increasingly, the value of data centre land is diverging from traditional commercial real estate. Whereas land values for logistics and light industrial use are largely based on the property’s geographical location relative to people and goods flows, the value of sites intended for data centre development is closely linked to available grid capacity. As a result, geographical proximity to specific points in the power grid becomes important, both in the existing grid and in planned future grid infrastructure. This reduces the supply of relevant sites compared with logistics and industrial land more generally.

Infrastructure costs also play a significant role in determining land values. Long distances to the nearest substation can result in grid contribution costs that run into hundreds of millions of NOK. In the market, sites located close to initiated or imminent grid reinforcement measures achieve higher values than sites located far from the same measures.

Zoning, and particularly the processing time required to obtain data centre zoning, affects land value, although this effect is less visible as zoning for the correct use is often included as a condition in the purchase agreement.

The conditions agreed between the parties relating to power and zoning, and the extent to which those conditions reduce risk, affect the value potential. This creates a wide range of outcomes for relevant data centre sites. Some are priced in line with local logistics land, while the most attractive sites may achieve a significant premium if they meet data centre developers’ strict requirements relating to grid access, time to market, drive times, labour market, risk assessments and other factors.

Conclusion

Power constraints in Europe and the emergence of AI factories have, in recent years, placed Norway on the map for large, professional and well-capitalised data centre developers.

The main limiting factor is the power grid. Major grid infrastructure investments are time-consuming, and the application queue for grid connections has grown rapidly. There is now 23 times more capacity in the queue than in all currently operational data centres combined.

Akershus Eiendom’s analysis indicates that approximately half of the projects in the queue or with reserved grid capacity are owned by players with strong execution capability and sufficient capital to build and own the centre themselves. The remainder require significant scaling of both organisation and capital. Going forward, we expect both consolidation and new partnerships in the market.

For landowners, the strong demand growth in the Norwegian data centre market means that properties with the right combination of power, fibre, land area and planning feasibility may see increased strategic value. The queue is long, but there are still opportunities to establish strong projects in the right locations.

Glossary

Statnett: Norway’s transmission system operator (TSO), which owns and operates the transmission grid.

MW – megawatt: A unit of power at a point in time. In a data centre context, MW is often used to describe the electrical capacity a project requires or has available.

MW IT load: The portion of a data centre’s power requirement that goes directly to IT equipment such as servers, storage and networking equipment. It is often used as a commercial measurement unit in data centre leasing.

TWh – terawatt hours: A unit of energy volume over time. 1 TWh equals one billion kilowatt hours and is often used to describe annual power generation, power consumption or power exports.

Transmission grid: The highest level of the Norwegian power grid, consisting of 300 kV and 420 kV high-voltage lines and substations.

Regional grid: The grid level between the transmission grid and the distribution grid. The regional grid transports power regionally and is often relevant for larger industrial customers and data centre projects.

Distribution grid: The lowest level of the power grid, transporting electricity from the regional grid to end users such as homes, commercial buildings, smaller industrial users and local businesses.

Substation: A facility that transforms electrical voltage between different grid levels, for example from the transmission grid to the regional grid.

Grid capacity: Available capacity in the power grid to accommodate new or increased consumption or generation without weakening security of supply.

Reserved grid capacity: Capacity committed to a specific project after the project has been assessed as sufficiently mature and capacity exists or will be developed.

Capacity queue: The queue for projects that have applied for capacity and been assessed as mature, but where there is no available capacity in the existing or planned grid.

Maturity assessment: The grid company’s assessment of whether a project is sufficiently concrete, documented and deliverable to reserve capacity or obtain a place in the capacity queue.

Grid contribution: A cost contribution payable by the customer for necessary grid investments, grid reinforcements or connection measures triggered by the project.

Powered land: A site with genuine or secured access to sufficient power capacity, often combined with appropriate zoning, fibre, drive times and other infrastructure required for data centre development.

Hyperscale: Very large data centres or data centre customers with significant and scalable capacity requirements, typically global technology companies and cloud platform providers.

Neocloud: A newer type of cloud provider delivering GPU-intensive compute capacity, often specialised towards artificial intelligence, machine learning and high-performance computing.

GPU - Graphics Processing Unit: A specialised processor capable of performing many calculations in parallel. GPUs were originally used for graphics and gaming, but are now central to artificial intelligence, machine learning and high-performance computing. In a data centre context, GPUs drive higher power requirements, denser racks and greater cooling requirements than traditional servers.