Market Views, CRE | Attractive Outlook for Retail

Strong fundamentals in Norwegian retail trade supported a clear recovery in the leasing market and increased investor interest in retail real estate in 2025. Although higher interest rates are expected to dampen consumption growth in the short term, both occupiers and investors appear to be looking through this near-term headwind, with solid activity levels in both the leasing and investment markets.

Increased Leasing Activity

Following an extended period of subdued activity, the second half of 2025 marked a clear turning point in the retail leasing market. Rising optimism among retailers led to a notable increase in demand for retail space. This development should be seen in the context of improved purchasing power and growth in retail consumption, combined with expectations of positive real wage growth and lower interest rates going forward.

Demand has primarily been driven by large, well-established international concepts, as well as Swedish fashion retailers. Several players have already entered the market, while the pipeline of potential entrants remains extensive.

Figure 1 – Selected recent international entrants to the Norwegian market

According to JLL, strategic expansion into underpenetrated European markets remains a key growth driver for retail. In this context, Oslo stands out as an attractive destination, underpinning expectations of continued demand growth from international operators.

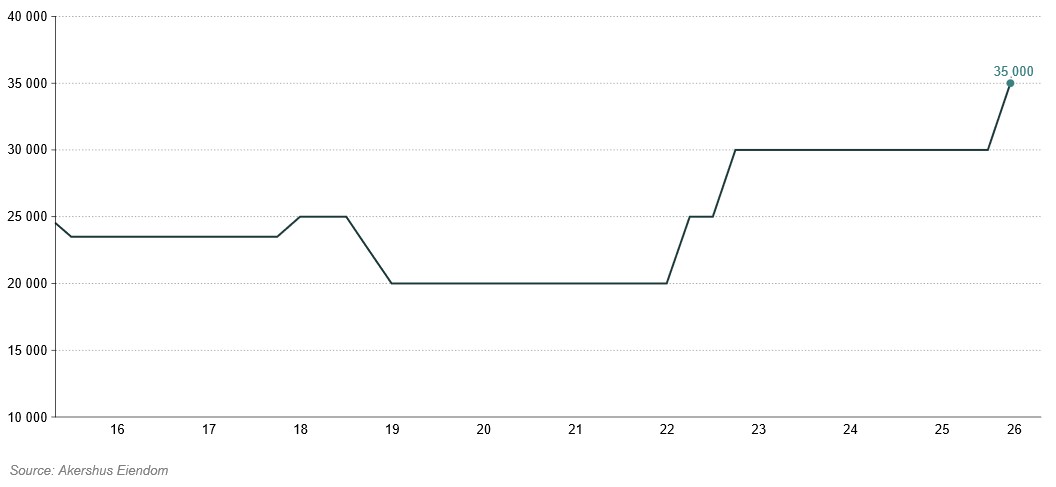

Market entry strategies follow a well-established pattern: initial presence in prime high-street locations in the capital, followed by expansion into secondary locations and shopping centres. In Oslo’s prime high-street segment, demand now exceeds supply, driving prime rents to NOK 35,000 per sqm. At the same time, rental levels remain highly polarised, with significant variations over short distances.

Figure 2 – Prime high-street rent levels, Oslo

Historically, increased activity in the high-street segment has acted as a leading indicator for broader recovery in the retail market. As such, there is reason to expect that demand growth will gradually extend to secondary retail locations, shopping centres and retail parks.

Short-Term Moderation

As outlined in the macroeconomic analysis, interest rate expectations have shifted, with higher rates now anticipated in Norway going forward. This is likely to dampen consumption growth in the short term. In addition, a stronger Norwegian krone may reduce inbound demand, which in recent years has been supported by a weak currency.

Despite this, leasing activity has remained robust in the first months of 2026. International operators appear largely to base decisions on long-term strategic considerations, with Norway continuing to be viewed as an attractive market. At the same time, long lead times in leasing processes mean that current decisions are only to a limited extent influenced by short-term volatility.

Should uncertainty persist or intensify, however, there is a risk that the recovery in the leasing market may lose momentum. Retailers are highly dependent on stable demand expectations, and prolonged volatility may lead to postponed entry and expansion plans. In such a scenario, leasing activity could weaken again.

Rising Transaction Activity – Still Selective

Positive developments in Norwegian retail, combined with increased leasing activity, have supported strong investor interest in retail real estate. Following a period of significant repricing, the segment has proven more resilient than anticipated, with stable physical retail performance and limited impact from e-commerce. Increased focus on portfolio diversification has also contributed to rising investor appetite. At the same time, retail appears attractively priced relative to other sectors in a challenging real estate market.

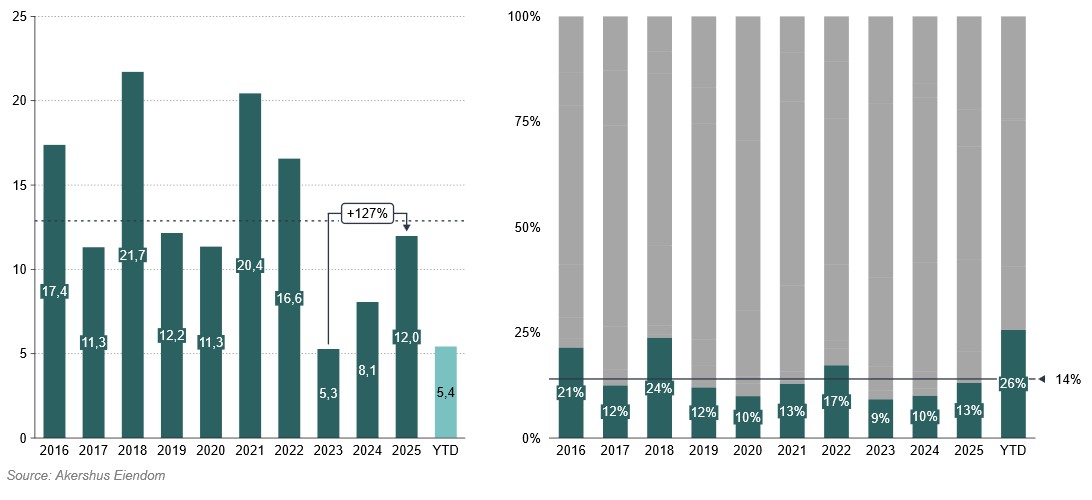

This has contributed to a recovery in transaction volumes over the past two years. In 2025, approximately NOK 12 billion of retail real estate was transacted in the Norwegian market, representing a significant increase compared to both 2023 and 2024. Retail accounted for just over 13% of total transaction volume, broadly in line with the 10-year average. Year-to-date, the share stands at 26% of total volume, well above the historical average.

Figure 3 – Transaction volume, retail (NOK and share)

The market remains clearly bifurcated. Prime assets across retail sub-segments attract strong demand and pricing, while assets with vacancy or repositioning potential are increasingly being priced based on upside. Currently, we observe strong interest in shopping centres, grocery-/retail park assets, and high-street retail.

Shopping centres represent the largest retail segment in Norway, historically accounting for 40–50% of total retail transaction volume. By mid-Q2 this year, the number of shopping centre transactions is already close to full-year 2025 levels, underlining increasing investor interest. A recent example is Aurora Eiendom’s entry into Trondheim through the acquisition of City Syd for NOK 2.15 billion.

Grocery and roadside retail parks have also stood out as attractive investment opportunities in recent years. This is driven by stable and long-term cash flows secured by strong tenants, resilience to e-commerce, and relatively attractive pricing. In an environment characterised by increased uncertainty, we expect continued strong investor interest in such defensive strategies.

Looking ahead, we expect a gradual increase in retail transaction volumes, supported by a robust leasing market and a larger supply pipeline. We observe that more investors are seeking exposure to high-quality assets in segments offering attractive returns and stable cash flows, making retail an appealing option. Although higher interest rates may weigh on overall sentiment in the transaction market, we nonetheless expect continued solid demand for retail real estate.