Market Views, CRE | Rising energy demand in the logistics sector

Artificial intelligence, urbanisation, automation and electrification are increasing energy demand in the logistics sector. As a result, access to power and proximity to grid connection points may become decisive factors when selecting warehouse locations.

Transport costs and labour remain central location drivers

As in the wider real estate market, the choice of warehouse and logistics facilities has traditionally been driven by location. For occupiers, the primary focus has been on transport costs and access to labour. This has led to attractive logistics parks being located close to major transport corridors and/or ports and airports, as well as near larger urban areas where people live. In today’s rapidly evolving market, however, secure and reliable access to power is increasingly emerging as a key factor when occupiers select future warehouse locations. While access to skilled labour and transport costs will remain central, access to electricity is becoming progressively more important in line with increased automation and the transition to an electrified vehicle fleet.

Power availability as a strategic location factor

This development is confirmed by a recently published report from Prologis Research (Prologis Supply Chain Intelligence Report 2026). The report shows that nearly 90 percent of respondents experienced energy-related disruptions in 2025, and that seven out of ten senior executives fear power outages more than any other form of operational disruption going forward. Despite this, fewer than one in three currently have access to backup power. Furthermore, 76 percent expect their power requirements to increase by 10–50 percent over the next five years.

This is influencing location decisions. According to JLL, as many as 90 percent of occupiers state that they are willing to pay a premium for locations with reliable energy infrastructure, marking a clear shift in how location is now assessed within the sector. This has already had a tangible impact in the advanced manufacturing market, where JLL finds that so-called “high-power leases” ¹ in Silicon Valley have been agreed at rental levels nearly 50 percent higher than other leases over the past three years, and 33 percent higher than rents achieved by the newest buildings.

1 JLL defines high‑power leases as lease agreements in industrial buildings with significantly higher electrical capacity than the market standard, typically properties with available capacity of around 4,000 amperes or more, enabling energy‑intensive operations and providing enhanced operational reliability.

Growing importance in the Norwegian market

We are seeing a clear increase in demand for sufficient and predictable access to electricity in the Norwegian leasing market. Although this has not yet been reflected in documented rental premiums for buildings with available power capacity, we observe a clear shift in occupier focus. An increasing number of tenants are requesting information on available capacity, grid connection options and redundancy, as well as access to backup power.

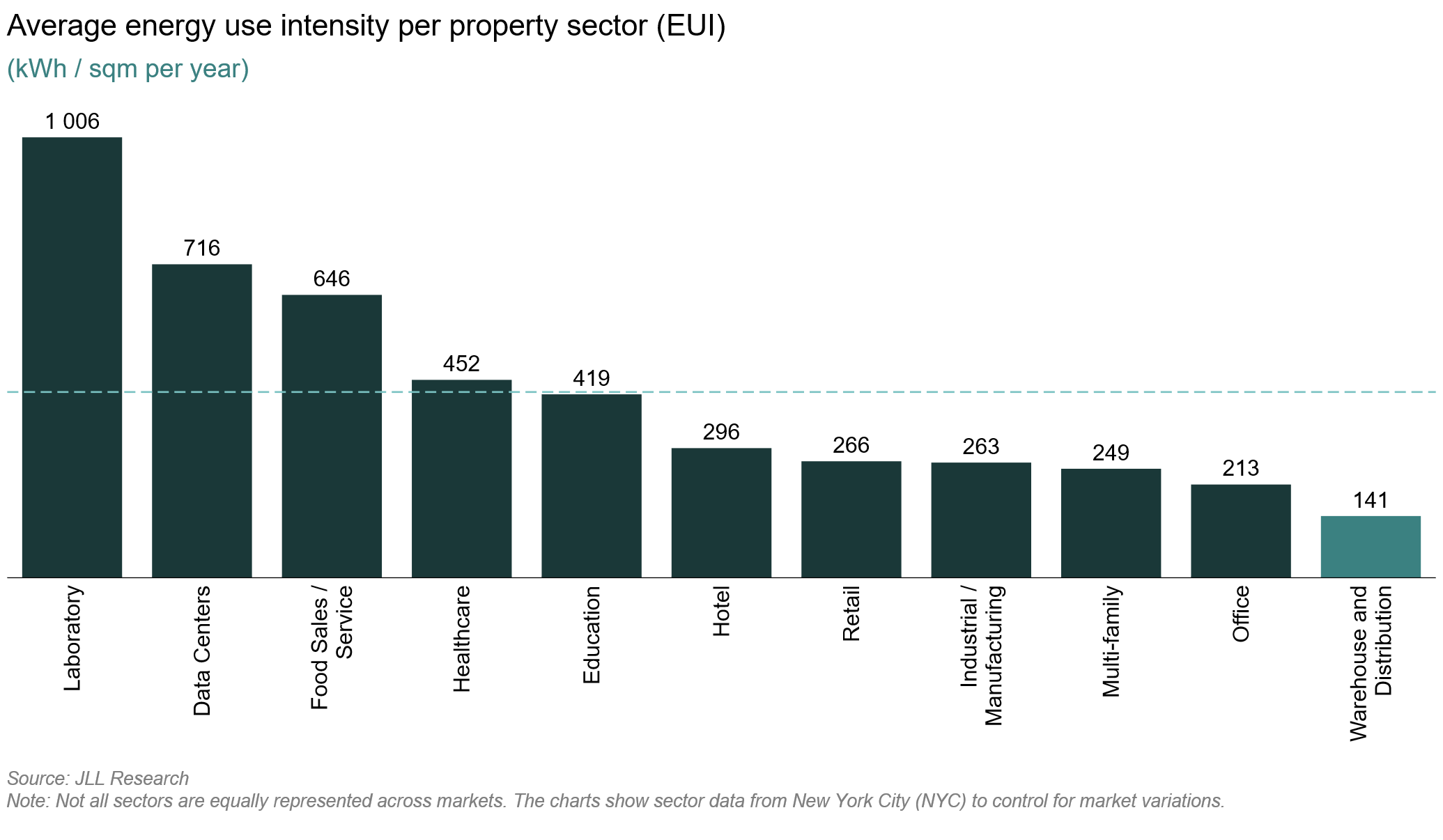

Figure 1 – Energy intensity varies across property sectors

While traditional warehouse buildings have relatively limited power requirements, properties associated with food production and distribution, as well as healthcare and pharmaceutical activities, are significantly more energy intensive. For occupiers handling chilled, frozen and other temperature-sensitive goods, uninterrupted power supply is critical. Even short outages can result in substantial financial losses due to temperature fluctuations, product damage and, in the worst case, full write-offs of goods.

However, we are now seeing a shift also among traditional warehouse users. Automation, electrification of vehicle fleets and internal logistics are contributing to electricity access increasingly being viewed as a critical operational factor. For occupiers, this is not only about current requirements, but also future scalability and flexibility. As a result, power availability is becoming a more important location factor than previously.

In addition, we observe that occupiers electrifying their vehicle fleets are increasingly requiring landlords to share part of the cost of upgrading a building’s power capacity to facilitate vehicle charging.

Constrained grid capacity

Although global evidence shows that occupiers are both willing and able to pay more for locations with sufficient power supply, this does not resolve the underlying constraint. In many markets worldwide, the primary bottleneck is no longer capital, land or labour, but available grid capacity.

This also applies to Norway. In several areas of Eastern Norway, grid capacity is already constrained. Limited power availability and long lead times for grid reinforcement are affecting both new developments and the further development of existing logistics properties. Statnett is planning extensive upgrades, but additional capacity is not expected to materialise until 2030–2035.

For logistics operators, this means that planning for local energy generation in cooperation with landlords is becoming increasingly important. Large, flat roofs make warehouse and logistics buildings well suited for solar installations that enable on-site power generation. In addition, solutions such as battery storage can help manage peak loads and enable charging of heavy electric transport vehicles. These measures can also relieve pressure on the public grid and enhance operational resilience by providing backup power in the event of outages. Such solutions are already widespread in larger European markets, including Sweden. In the Norwegian market, this is becoming increasingly important for occupiers, but implementation depends on landlords being willing to participate in the required investments.

Conclusion

Access to electricity may increasingly become a differentiating factor in the Norwegian logistics and light industrial market. Sites with secure and reliable grid capacity, provision for depot charging, and opportunities for local energy generation and storage may offer a clear competitive advantage going forward. At the same time, occupiers in existing buildings are likely to expect more active involvement from landlords in relation to grid connections, capacity upgrades and energy solutions. Over time, this is likely to result in a more pronounced market bifurcation, where sites and buildings with sufficient power availability achieve stronger demand and higher rental levels.