Market Views, CRE | Outlook for 2026 - What will drive the transaction market going forward?

Looking ahead, we are unlikely to receive support from the financial markets. Nevertheless, we expect activity levels to remain broadly in line with last year. In 2026, consolidation, diversification, and strong underlying fundamentals are expected to be the primary drivers of activity in the Norwegian transaction market.

The Transaction Market in 2025

Total transaction volume in 2025 amounted to NOK 91 billion, up nearly 15 percent year‑on‑year, supported by several large transactions that lifted overall volumes. The market was characterized by a clear bifurcation, which we expect to persist into 2026. Prime assets across property segments, offering strong cash flows in attractive locations, continue to experience solid demand, while lower‑quality assets in less favorable locations face a more challenging market environment. Throughout last year, unlevered investors dominated demand for top‑tier assets and were also a key driver of both liquidity and pricing in the market.

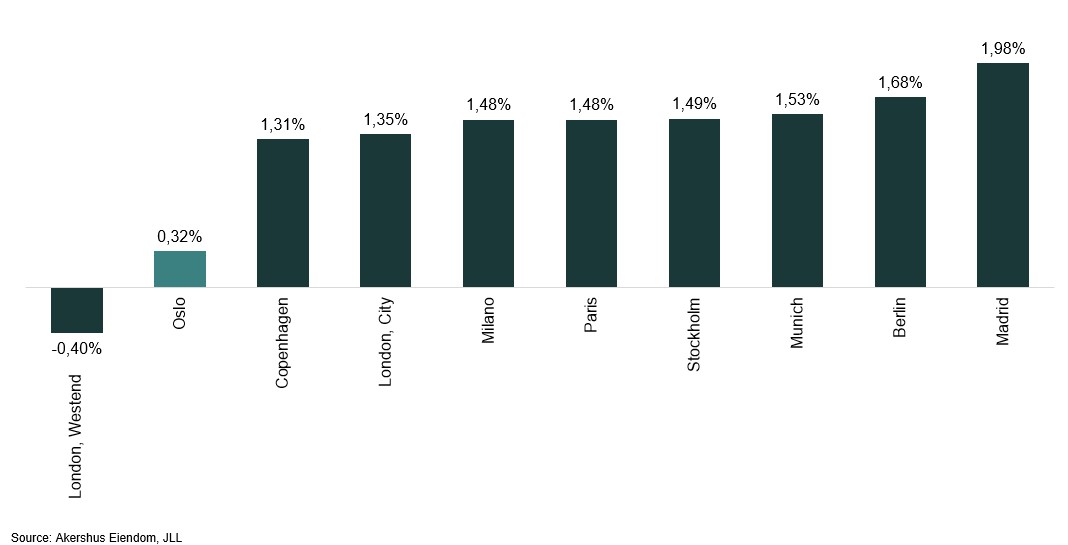

As outlined in the macro section of this analysis, the financial markets are unlikely to provide significant tailwinds going forward. Expectations of persistently high interest rates in Norway remain challenging for many participants, particularly within the office segment. Norway currently has one of the lowest office yield gaps in Europe, which may further limit activity from international investors. In addition, a potential correction in equity markets could reduce support from an asset allocation perspective. Despite this, we expect transaction volumes in 2026 to remain broadly in line with 2025 levels.

Figure 1: Yield gap – selected European cities

Consolidation

Consolidation is expected to be a key driver of transaction activity in 2026. Compressed margins, higher capital requirements, and increasing demands related to operations, reporting, and ESG make it difficult to remain competitive without sufficient scale. Larger players benefit from structural advantages through lower unit costs in operations, procurement, and administration, as well as more efficient asset management enabled by standardized processes and shared system platforms. In a market with limited tolerance for operational missteps, scale is increasingly a prerequisite for delivering stable returns.

Financial factors further reinforce this trend. Access to capital and financing terms favor players with strong balance sheets and diversified portfolios. Larger platforms consistently achieve lower margins, better financing terms, and greater flexibility in their capital structures, enhancing their ability to act in a market characterized by lower liquidity and high capital intensity. Consolidation therefore not only generates cost synergies, but also strengthens financial resilience and the ability to execute transactions when smaller players are forced to sell or restructure.

This development is already evident in the market. The merger between Aspelin Eiendom and Reitan Eiendom in Oslo, at an estimated valuation of approximately NOK 19 billion, illustrates how larger players are seeking increased scale, financial capacity, and operational strength. Similarly, Spleismark Næring has recently invested in Lerka Eiendom, strengthening investment capacity and enabling further growth. At the same time, several additional transactions are known to be in progress, involving new ownership structures established through mergers, asset contributions, and strategic partnerships. For larger, professional investors, this represents a clear opportunity set, while small and mid‑sized players increasingly risk cost disadvantages, weaker bargaining power, and marginalization in a more standardized and professionalized market.

Diversification

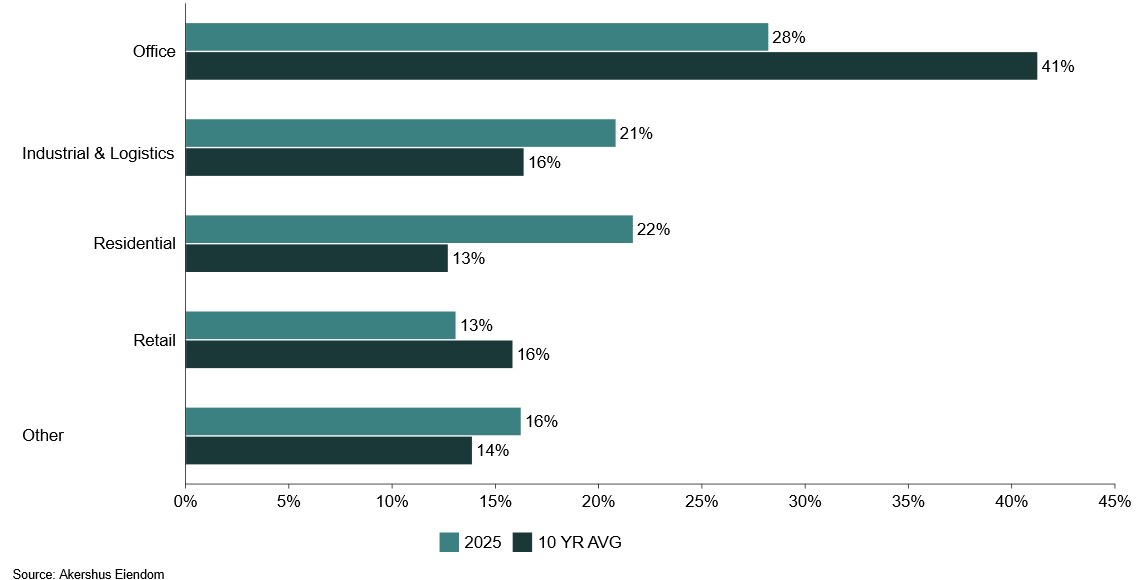

Diversification has become increasingly important in the transaction market following several years in which office assets were the dominant segment. Historically, office properties have accounted for a significant share of transaction volumes in Norway, but activity has gradually declined since the pandemic and was lower last year than in previous periods. Investors with a traditional office focus have increasingly expanded their investment mandates to include other segments. Notably, KLP has in recent years made its first investments in both logistics and residential rental housing, illustrating a clear strategic shift toward broader exposure and more diversified cash flows.

Figure 2: Transaction volume in 2025 vs.10‑year average

This trend is further supported by increased activity within retail and logistics following a period of subdued transaction volumes. Toward the end of last year, OPF acquired Bekkestua Senter, while PKH completed the acquisition of Smalvollveien 65 in Alnabru. At the same time, the supply side remains characterized by low liquidity, and when high‑quality assets are brought to market, we observe strong engagement from the most robust capital sources. Higher yields in alternative segments compared to office, combined with a limited supply of attractive assets, intensify competition and drive broader allocation across property segments.

Fundamental Drivers

Across most segments, fundamental conditions are characterized by an imbalance between supply and demand in the leasing market. Low construction activity across segments—driven by high construction and financing costs as well as increased capital tied up in development projects—has limited the supply of new, high‑quality space. This has reinforced a pronounced flight‑to‑quality, with tenant demand concentrating on existing properties in strong locations with adequate functional standards. In the office segment, this has resulted in persistently low vacancy for prime buildings, even as overall vacancy rates in Oslo have increased. Concerns regarding a permanent reduction in office space demand due to remote work have largely subsided; however, stricter tenant requirements, substantial capex needs, and technological changes place higher demands on building quality. Limited new supply in Oslo’s central business districts through 2029 further supports this market dynamic. For investors, this underpins a selective approach to the office market, where quality and location are critical determinants of risk profile and return potential.

Figure 3: 2026 forecast supply completions vs 2021-25 peak

In the residential segment, long‑term fundamentals remain supportive, but the market continues to face challenging framework conditions. A persistent imbalance between supply and demand, combined with an anticipated housing shortage, provides a structurally positive backdrop. However, high construction and financing costs make new projects difficult to execute. At the same time, development projects tie up significant capital over extended periods, prompting asset sales and restructurings rather than new activity. Given elevated costs, substantial capital intensity, and limited project feasibility, the residential segment currently appears more challenging in the transaction market than several alternative segments.

In the current market environment, logistics, retail, and hotels stand out as the segments with the most attractive fundamental conditions. Demand for logistics is supported by increased focus on resilient supply chains, investments in defense‑related industries, and growing interest from pension and life insurance capital, although rental growth has moderated compared to earlier periods. Within retail, both shopping centers and big‑box retail have delivered solid turnover growth and demonstrated greater resilience than previously anticipated, with more limited impact from e‑commerce. The hotel segment has simultaneously experienced very strong performance in terms of average daily rate (ADR) and revenue per available room (RevPAR) since 2019, supported by a weak Norwegian krone and strong demand. Taken together, these factors create an attractive investment landscape, offering competitive risk‑adjusted returns across these segments.