Market Views, Macro | Limited Support from Financial Markets

Market participants expect interest rates in Norway to remain elevated over the coming years. At the same time, concerns about a potential correction in equity markets have intensified. In our view, these factors represent a risk to commercial real estate pricing going forward.

Outlook for persistently high interest rates

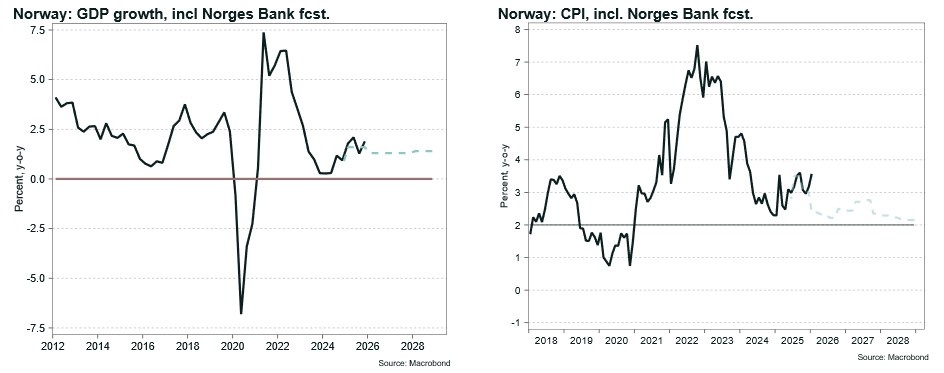

Norges Bank’s interest rate forecast from December implies three policy rate cuts over the next three years. The central bank has also indicated that it envisages cutting rates once or twice in 2026. However, recent data on GDP growth and inflation have led market participants to believe that no rate cuts will materialise this year after all.

As things stand today, mainland Norway GDP growth has recovered to broadly normal levels, while inflation has been materially higher than expected and appears to be entrenched at around one percentage point above the inflation target. This is likely to cause Norges Bank to exercise caution when it comes to easing monetary policy.

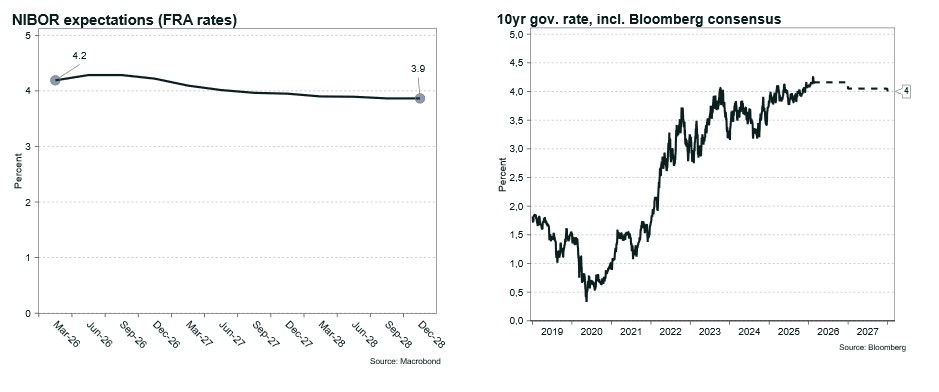

NIBOR is currently at 4.2 per cent, while the policy rate stands at 4.0 per cent. Pricing in the FRA market suggests that only one rate cut is expected from the central bank over the next three years, implying a decline in NIBOR to around 3.9 per cent.

Under normal conditions, long-term interest rates exceed short-term rates. At present, the 10-year government bond yield stands at 4.15 per cent, broadly in line with NIBOR. Consensus expectations indicate that the 10-year government bond yield will decline only marginally, to around 4.0 per cent, over the next two years. Swap rates typically track government bond yields with a modest spread.

Overall, market participants do not expect interest rates to fall materially from current levels. Based on Norges Bank’s assessment of what constitutes a neutral interest rate for the Norwegian economy, current levels are also relatively close. According to the central bank, a normal NIBOR rate lies in the range of 2.5–3.75 per cent.

Elevated equity market valuations

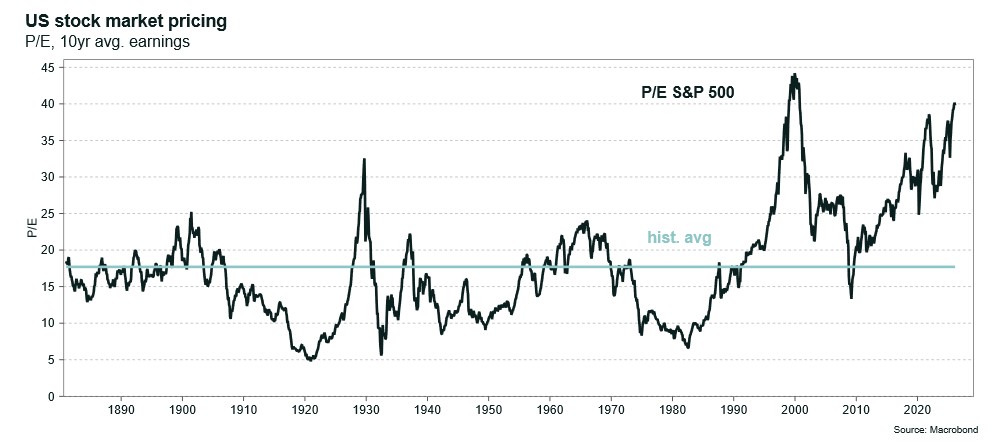

Despite persistently high interest rates in both Norway and the United States, equity markets have performed strongly over the past three years, particularly in the US. In Norway, equity market gains have been supported by strong results in the energy sector and a weaker Norwegian krone. In the US, the pronounced increase in valuations has primarily been driven by the technology sector and developments related to artificial intelligence.

Valuations in the US equity market have become increasingly stretched. Measured as share prices relative to average earnings over the past ten years for S&P 500 companies, this metric has not been higher since just prior to the bursting of the dot-com bubble in the early 2000s. As a result, there is growing concern in the market that the AI bubble could burst, triggering a broader equity market correction.

Implications for commercial real estate

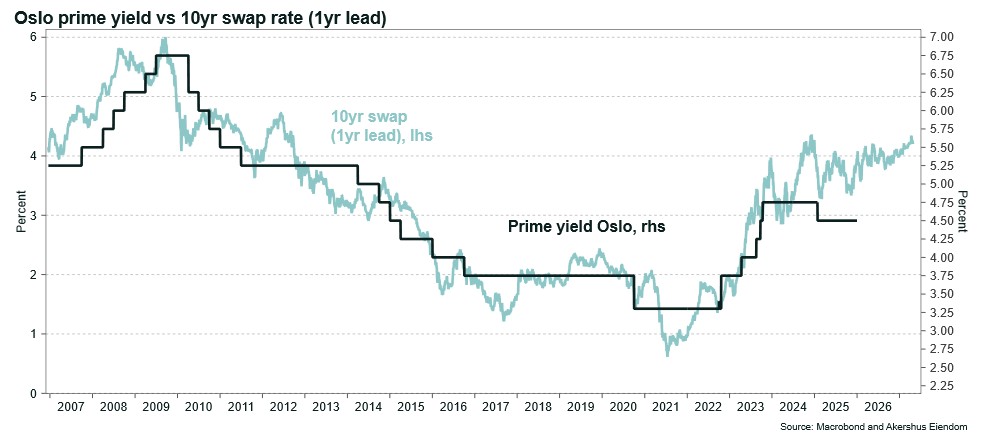

Many Norwegian investors, including life insurance companies and pension funds, have significant exposure to the US equity market. Several of these investors are also major participants in the real estate market. Over the past two years, we have observed that an unusually high share of prime yield transactions in the commercial property market have had life insurance companies and pension funds on the buy side. One of the key drivers has been the strong performance of equity markets, which has prompted these investors to increase their allocation to real estate for portfolio rebalancing purposes. Should equity markets experience a correction going forward, this consideration would work in the opposite direction.

Life insurance companies and pension funds, which typically invest with a high proportion of equity, have also contributed to compressing property yields despite the elevated interest rate environment. This has led to a breakdown in the historically strong correlation between property yields and long-term interest rates. Based on the relationship with interest rates over the past 20 years, commercial property yields are currently unusually low.

In our view, the prospect of persistently high interest rates, combined with stretched equity market valuations, represents a risk to pricing in the commercial real estate market in the period ahead.