Logistics market update Q3 2019

High activity in logistics development where tenant demands keep increasing, and scarcity of central land plots drive attractivity for the larger hubs outside Oslo. Transaction volume is down compared to 2018 due to few investment-grade assets in the market. Prime rent levels remain stable in the greater Oslo area.

Fuelled by continuous development in distribution efficiency, E-Commerce and last-mile logistics, the activity in the greater Oslo logistics market remain high moving towards 2020. Proximity to effective intersections with the main highway E6 is more important than ever and will remain a key selling point towards logistics operators.

A scarcity of available and buildable land plots, especially close to Oslo, is increasing the attractiveness for the logistics hubs located in the eastern north-south axis, in other words from Oslo towards Oslo Airport, and south toward the Moss region. Most new development projects are located in or close to the logistics hubs on the eastern axis. The most attractive locations are, however, still in short distance to the national cross-dock rail and road terminal Alnabruterminalen at Alnabru.

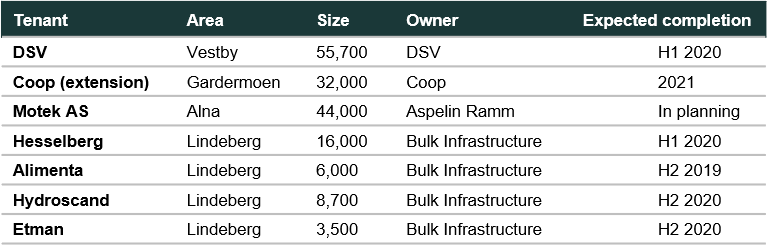

Confirming the outwards pressure from Oslo is the former agricultural land plot at Lindeberg, just north of Berger which is in the process of being transformed to a smaller logistics hub. Over the past year one has seen 4 new signings in the area containing Hesselberg, Hydroscand, Alimenta and Etman.

Another hub with high development activity is Vestby, where Prime Cargo recently opened Norway’s largest 3PL facility comprising 44,000 sq.m terminal and warehouse. DSV recently purchased a 110,000 sq.m land-plot from Ferd Eiendom on the south side of Vestby, where they will construct a 55,700 sq.m warehouse/terminal with estimated completion in mid-2020. IKEA plans to develop a fully automated warehouse to facilitate for increased traffic from E-Commerce at Vestby east. Construction start is currently undecided.

We believe that the development activity will stay strong in the hubs as demand is increasingly put on landlords to facilitate for future flexibility to expand on property. At the same time, logistics assets are becoming more and more complex as fully automated warehouses and cross-dock systems are becoming the norm.

The prime rent estimate for logistic/warehouse properties with no or few tenant-specific investments is still at NOK 1,200. This rent is mainly obtained in the Alna area.

Transaction activity

The development in the transaction market has been slower than previous years, and 13 logistics/terminal properties in Norway amounting to bNOK 2.12 have changed hands per October 2019. The most active buyers of logistics properties year to date are closed-ended funds looking for long secure cash-flows. Second is Norwegian property funds, especially specialist funds with a strong focus on logistic properties. Compared to a full-year transaction volume of bNOK 7.9 in 2018, 2019 is lagging. However, we believe that both volume and number of transactions would be higher if more investment-grade properties were presented to the market.

The prime yield estimate is 4.75-4.875% for 10-year investment grade assets. Substantially longer leases may achieve lower yields. The prime yield estimate is relevant for properties located from Berger to Vestby. Slightly higher yields are seen north or south of this corridor.